A security deposit is a one-time, refundable payment made by a tenant before moving into your single-family rental home. It acts as financial insurance against potential damages, unpaid rent, or cleaning fees incurred during their tenancy. Security deposits are large sums of money, and constantly change hands in the single-family rental (SFR) community.

Traditional security deposits are standard in the industry but aren’t ideal for everyone. They can typically cost over the first month’s rent for residents and can be a hassle to manage for property managers and investors.

If you’re familiar with our Triple Win approach and resident benefits, you won’t be surprised to learn there’s a different way.

Security deposit alternatives typically allow tenants to pay their security deposit in installment payments instead of a lump sum before their occupancy of a rental property. Continue reading to find out more about the different types of security deposit alternatives, their cost, and their pros and cons to help you choose the one that works best for you.

Related: How to Write a Security Deposit Return Letter + Free Template

Types of Security Deposit Alternatives

Security deposit alternatives can be achieved through pure insurance, surety bonds, ACH authorization, or an in-house program. Property managers may choose these types of alternatives because they aim to lower the barrier to rental for residents. As a result, this lower barrier increases the ROI for the owner and boosts the PMC’s bottom line.

These options, however, are not a one-size strategy. They can vary based on the business size, strategy, and state and local laws. In addition, there are several different ways to apply. For example, insurance, surety bonds through a bond company, and ACH authorization are all available through third-party vendors, which are increasing in popularity.

Next, we’ll walk through each of these security deposit alternatives.

Pure insurance

This is exactly what it sounds like. Instead of a deposit covering potential damages, the resident takes out a policy with an insurance company to cover any damages. The resident pays a small premium, and on move-out, the policy covers any damage to the property up to a certain amount.

Pure insurance is great for the resident, who pays a premium and then bears no financial responsibility for damages after move-out.

Inherent in that approach, however, is a flaw that makes the pure insurance play tough to buy into as the industry's future. It doesn't incentivize the resident to take care of the property, as they won't owe any additional money for any damage they cause. This flaw leads to higher premiums, leaving insurance as a less effective way to keep costs down.

Surety bond

The surety bond business model is not new. Still, it's become more popular as vendors have modernized the enrollment experience thanks to over $150M of VC investment into the category.

Surety bonds are agreements between two parties managed by a third party, known as the surety. In the case of property management, the contract is between you as the property manager and the resident. It states that the resident agrees not to damage the property and agrees to cover damages should they be responsible. In case of a contract breach at the end of the lease, the surety pays out the sum required to the property manager, then bills the resident the cost of the damages.

Surety bonds attempt to incentivize the resident to take care of the property, which is more than a pure insurance program will do, but there's not a definitive set of evidence yet that this is highly effective. It's still a challenge to educate some residents that this isn't an installment plan or insurance product. In many cases, that falls on the property management team.

Another concern with the surety bond model is the post-move-out collection results. The majority of damages due from the resident never get collected, which leaves the model with potential recourse ahead:

- Vendors figure out how to collect a higher percentage

- Vendors increase monthly pricing

- Vendors expand into other, more profitable products

- Less reliable claims payouts

- Layoffs or other financial controls

- More investment was requested for more runway

The jury is still out on whether surety bonds have the unit economics to win the category.

ACH authorization

The ACH (Automatic Clearing House) authorization is a popular alternative. It mirrors the method hotels have used for years to compensate for incidentals and applies it to long-term rentals. Residents permit a financial institution to directly draft money up to a certain amount to cover damages and draw from your bank account.

The ACH authorization does check the box of incentivizing proper treatment of the home, and the vast majority of money due from claims is collected. So far, this method seems to be getting the best results in post-move-out collections.

A fair critique is not 100% of residents qualify for this, and the ones that don't must pay a traditional deposit, so it isn’t a complete solution in some people’s minds.

In-house program

Todd Ortscheid, CEO of Revolution Rental Management, built his alternative program in-house. Ortscheid spoke on this topic in an episode of Triple Win LIVE in February.

“We offer the resident two different options. You can either pay the security deposit amount based on your [application] score, or the alternative is you can pay a monthly security deposit waiver fee,” says Ortscheid. “What the waiver fee is doing is buying you the privilege of not having to pay a security deposit upfront.”

Ortscheid clarifies that his implementation of this program is neither insurance nor a refundable installment towards a security deposit. However, there is debate among other PMs and their attorneys about what compliance risks there could be here. Some property managers also struggle to get comfortable with the financial liability.

Related: Benefits of Property Management Outsourcing Services

When deciding to outsource or DIY, we recommend considering three things:

- How much of a difference can scale make now? Over time?

- How large is the skill or expertise gap here? Over time?

- Is this the best investment of my time? Will it be later?

Security Deposit Alternative Companies and What They Offer

The traditional security deposit is the OG of rental insurance, a reliable one-time payment typically equal to one month's rent. It works like a financial handshake between the resident and property manager/owner, acting as a safety net for unpaid rent or damages beyond normal wear and tear. While it carries no monthly cost for residents and offers full refunds for responsible renters, it also doesn't offer revenue sharing for investors or the flexibility of newer alternatives.

Here's what to expect from a traditional security deposit product, and the baseline we'll be comparing alternatives to:

- Model: Traditional

- Up-front cost to resident: Equal to established cash deposit

- Monthly cost to resident: None

- Unpaid rent & damage coverage: Equal to established cash deposit

- Revenue share with property investor? N/A

- Payments refundable to resident? Yes

- Resident held accountable for funds? N/A

We reached out to Peter Lohmann, co-founder and CEO of RL Property Management, to get the rundown on security dispositive alternative products. Here are some of the most popular security deposit alternative services, the type of product they offer, and the pros and cons of each.

Note: The major downside for most of these security deposit alternative products is that they focus on multi-family rental (MFR) communities rather than single-family rentals (SFR). Most also have nonrefundable fees.

1. LeaseLock

LeaseLock is a popular security deposit alternative program. Here’s how they stack up:

- Model: Lease Insurance

- Up-front cost to resident: None

- Monthly cost to resident: $29 for standard plan

- Unpaid rent & damage coverage: $5,000 for standard plan

- Revenue share with property investor? No

- Payments refundable to resident? No

- Resident held accountable for funds? Yes but Lease Lock says they don’t pursue

2. Obligo

Obligo is a billing authorization alternative to security deposits. Here’s how they stack up:

- Model: Bill Authorization

- Up-front cost to resident: First year’s total fee (variable)

- Monthly cost to resident: None

- Unpaid rent & damage coverage: Equal to established cash deposit

- Revenue share with property investor? No

- Payments refundable to resident? No

- Resident held accountable for funds? Yes

3. Rhino

Rhino offers the surety bond model for security deposit alternatives. Here’s how they stack up:

- Model: Surety Bond (non-pooled)

- Up-front cost to resident: None

- Monthly cost to resident: Variable

- Unpaid rent & damage coverage: Equal to established cash deposit

- Revenue share with property investor? Yes, if over 10K units

- Payments refundable to resident? No

- Resident held accountable for funds? Yes, but Rhino says they don’t always pursue

4. TheGuarantors, Jetty, and SureDeposit

These three companies – The Guarantors, Jetty, and SureDeposit – all offer an alternative to security deposits in the form of a surety bond. Here’s how they stack up:

- Model: Surety Bond (pooled)

- Up-front cost to resident: 17.5% of month’s rent

- Monthly cost to resident: None

- Unpaid rent & damage coverage: Equal to established cash deposit

- Revenue share with property investor? No

- Payments refundable to resident? No

- Resident held accountable for funds? Yes

The Cost of a Security Deposit Alternative

Security deposit alternatives costs don’t necessarily save money for the resident, but they offer a choice that many residents prefer – not giving up a big chunk of cash right at the start.

In general, the cost structure for security deposit alternative companies is either a low monthly fee or an annual fee. For most PMs, you can include the cost in a Resident Benefits Package, or it’s billed directly to them by a vendor. The cost can depend on the property's value, the rent and deposit amount, the resident’s credit, etc.

Fees are calculated based on the amount of rent, amount of deposit, credit score of the renter, and the value of the client. Security deposit alternative fees can often be as low as 5% of rent. So, for a rent of $1500 a month, a resident might pay: $75 per month (5%). In some larger apartment communities, residents may pay even less – typically $8-$30 per month.

Advantages of Security Deposit Alternatives

The concept of a security deposit alternative is that it helps lower the barrier of entry for residents who may not want to put down a massive one-time chunk of cash – and it helps protect the investor by filling vacancies more quickly, and incentivizing good care of the property.

Here’s a breakdown of more specific advantages.

1. Avoid large deposits for residents

Ortscheid says: “When I first started doing this, my assumption was the only people who will take this are the people with the worst scores.

“What we actually found was our very first person who signed up for it was someone with an 800+ credit score. He was the CEO of a publicly traded company and had millions in the bank. So I asked why he took the waiver option, and he said, ‘I would rather pay monthly than give you a big chunk of my money.'”

2. Get more options

All of these programs can be relatively simple to administer and offer choice to the resident. They can choose options and payment methods like credit cards, ACH, etc.

According to Ortscheid: “About 70% of the people we rent to now select the security deposit waiver option.”

Giving residents more options helps them feel more secure and in control and boosts their satisfaction overall.

3. Reduce vacancies

Perhaps the investor sees the most significant win from security deposit alternatives. And, given the PM’s fiduciary responsibility to the investor, an investor win is usually a win for you.

The biggest thing here is the attractiveness of the program to the resident. A security deposit alternative is something you can and should advertise in your listings. It adds a differentiating factor to your listing that moves the needle for many prospective residents, which helps keep your days-on-market low. Revolution Rental Management has been sitting at an average of about ten days on the market over the last year. And as we all know, minimal vacancy equals increased ROI for investors.

4. Get fewer damage claims at move-out

Additionally, some property managers claim the lack of a deposit drives fewer damage claims at move-out. This reduction in claims helps to protect the investor’s assets more than a deposit does.

Again, this may seem counterintuitive, but Birdy Properties reports this scenario playing out since they moved away from security deposits two and a half years ago.

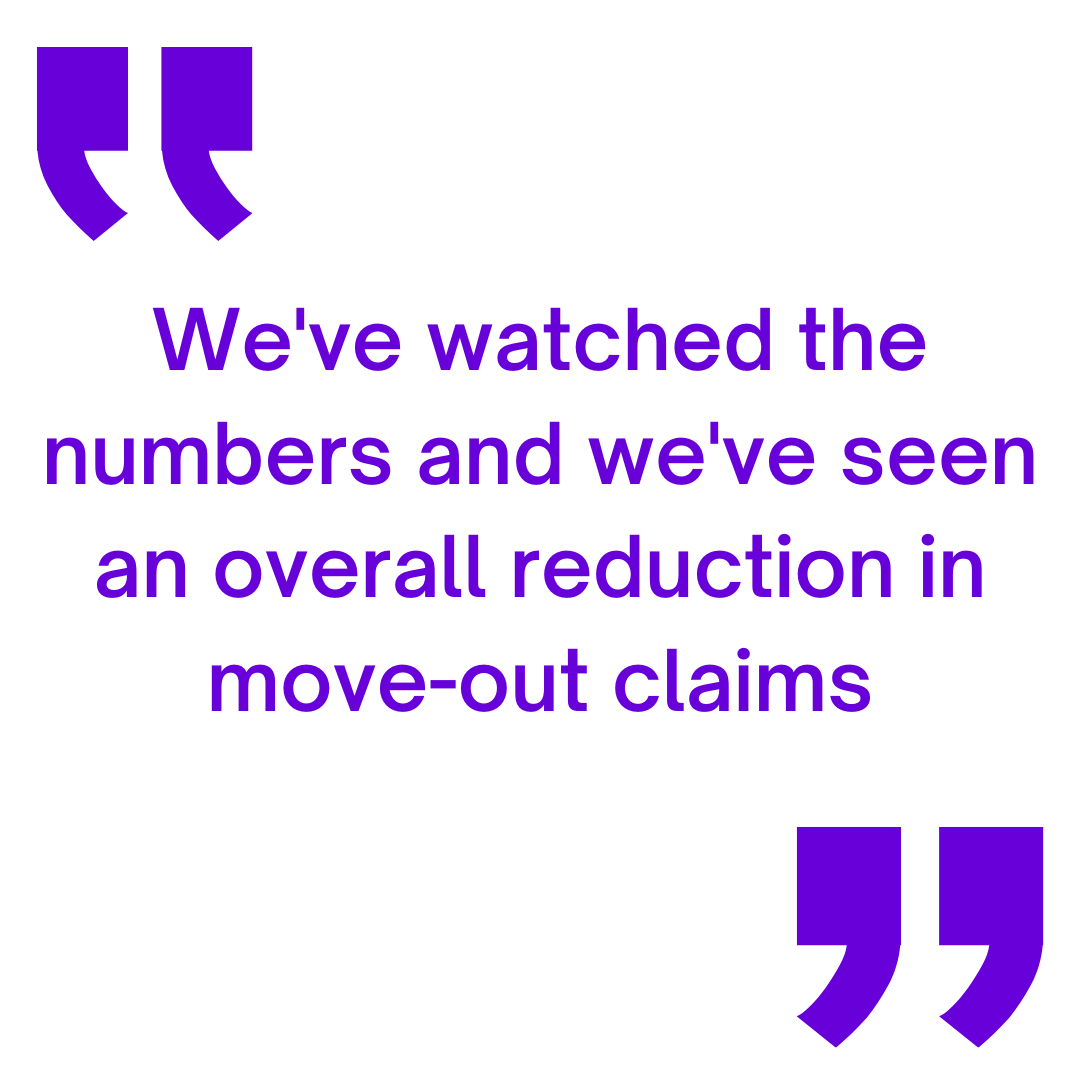

“There is this philosophy out there from residents. Most people believe ‘you’re not going to give me my money back. And since I’m not getting my money back, I’m not going to clean up too well because if I do all that work, you’ll still keep my money anyway. Well, now, you were nice enough to let me move in and not have to give you all this money. Everything has gone well, and now it’s time for me to leave and I can recognize that if I don’t leave the property in good shape, I’m going to have to pay for it.’”

“We’ve watched the numbers,” continued Birdy. “We have seen a reduction in overall move-out claims. What it’s costing to turn a property over has gone dramatically down, and we have almost eliminated the turnover cost to the owner. That is the most vulnerable time for us as property managers because that’s when the investor decides if they want to keep this asset any longer.”

The speed with which Birdy Properties can roll in another resident with minimal costs keeps the property investors happy, which prevents the PM from losing inventory while maintaining great service and relationships with the client.

This great relationship comes from a service residents love, so it all works together to benefit every party. Best practices are developing that will drive triple-win experiences.

Disadvantages of Security Deposit Alternatives

Of course, there are also disadvantages to security deposit alternative services. These issues may affect your residents' overall experience or your investor's satisfaction with their margins. Before signing up for any alternative security deposit product, you need to be sure you know what you’re getting into. Do your research and ask questions to evaluate things like: what happens if a resident ends their lease early; what damages are owed after move-out and who pays them; how to dispute charges; monthly or yearly fee obligations; etc.

Here are a few disadvantages to keep in mind.

1. Payments are not refundable

While the advantage to residents is that they don't have to pay it all right away, the disadvantage is that they won't be refunded for their payments.

2. Disputes may be more difficult to resolve

Since security deposit alternative programs involve a third party, you must involve another agreement with the lease and contracting stage. If there is an eventual dispute, it may be tough to get it resolved. Residents may not be held accountable in the way you and your investor need. Or, from the resident side, they may not get the service they want.

3. Security deposit alternatives don't save money

Some products may seem like they're advertising dollars saved. But ultimately, these alternatives aren't intended to save money. They simply help residents keep money in their savings for a longer period of time, rather than making one big deposit all at once.

Despite these disadvantages, we've seen security deposit alternatives pick up in popularity recently. As long as residents, investors, and PMCs know exactly what is and isn't promised, it can be a benefit to everyone involved.

How 1,000+ Professional Management Companies Create Triple Win Experiences

Security deposit alternatives are an innovative solution that solves problems for residents, investors, and property managers.

- For residents: A quality alternative lowers the barrier for residents and gives them more choice and agency in the rental process.

- For investors: A quality alternative can boost your listings’ marketability and reduce vacancy costs.

- For property managers: A quality alternative with more relevance for residents and investors – creates new value with an opportunity to monetize and eliminate the administrative pains of traditional deposits.

That’s what we call a triple win! Learn more about how we create resident experiences that people pay and stay for – and share your trips and tricks in our Facebook Group!

Topics: